Loading poster...

The current situation

Flood creates more losses than any other natural catastrophe peril, but is one of the least insured perils. Uninsured flood losses have exceeded those covered by insurance in many recent flood events.

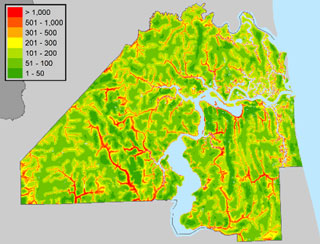

Flood risk varies over short distances, and a successful risk classification plan needs to accurately price this risk. Milliman is one of the first companies to develop sophisticated flood insurance solutions and has extensive experience addressing the challenges inherent in this work.

What we do

Milliman is at the forefront of innovation in flood insurance.

- Concurrent with the recent developments in flood insurance modeling and data availability, our consultants have developed independent flood rating and underwriting structures for private insurers.

- We are recognized global experts in property insurance ratemaking, with specialists to help insurers measure and manage the unique risks associated with catastrophe-exposed property risk.

- We employ competitive analysis to support pricing and profitability decisions, and sales and marketing strategies.

- Our experts are experienced in assessing and navigating the regulatory landscape. For admitted carriers, the ability to underwrite and price flood insurance profitably is dependent on state regulation, which varies widely across the US.

- We can assist with the implementation of catastrophic rating plans. We can create manuals and GIS layers, and assist with IT issues that may arise.

- Our team has performed in-depth statutory research and feasibility studies for insurers and reinsurers considering entering the flood insurance market.

- We have extensively reviewed storm surge catastrophe models and inland flood models, and have developed a variety of approaches to the area of flood insurance rate structures.

- Our consultants are recognized as thought leaders in flood insurance, and have presented on catastrophic risk rating and flood rating at numerous industry conferences. We are currently providing actuarial consulting services as part of a program to redesign flood insurance products across the NFIP.

Our tools

Bungalow: Prebuilt, customizable flood insurance solution

Milliman Bungalow is a complete, modern rating solution for insurers to quickly and cost-effectively build a profitable flood business.

Key features:

- Matches price to risk at the highest resolution in the industry

- Powered by the KatRisk SpatialKat flood models

- Flexible, low cost options for start-up and growing companies to avoid development and regulatory costs

- Designed for easy customization, Milliman’s experienced flood and GIS experts can tailor Bungalow to your needs

PinPoint: Prebuilt geospatial solution

Milliman’s PinPoint delivers relevant geographic rating insights to your system at the point of decision through a simple API.

Key features:

- Granularity and unique data drives more accurate rates

- Returns geographic insights customized to your rates and rules

- Milliman geographic and actuarial experts ready to tailor and support

Pixel

Pixel™ is a web-based, interactive premium comparison platform that helps companies quickly understand their rating positions and make informed decisions. The software incorporates:

- Market baskets (see below) or company-specific data, such as quotes

- Competitor premiums and modeled losses at the risk level

- Geospatial information and maps

- Data exploration and visualization

- Advanced analytics

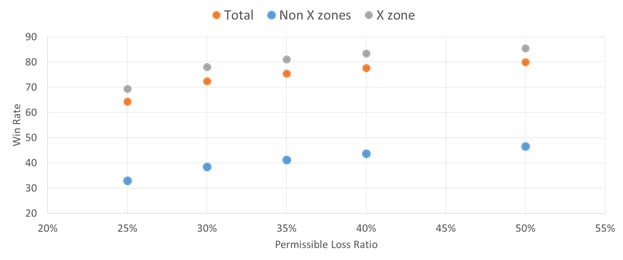

Test sensitivity of key metrics to assumptions

Example: Win Rate by Permissible Loss Ratio

|

Flood pricing structures |

|

NFIP clone |

Risk-level modeling |

Grid rating plan |

Refined rating plan |

Market Baskets

To reduce time and data required to enter the flood arena, Milliman has developed market baskets. These are portfolios of hypothetical risks with realistic distributions of characteristics used for property and flood insurance pricing. They include:

- Data on realistic properties with location-level specificity

- Critical risk factors based on advanced geospatial measurements

- Competitor premiums and catastrophe model losses for selected states/products

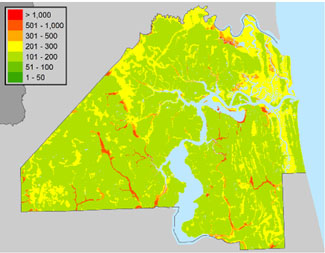

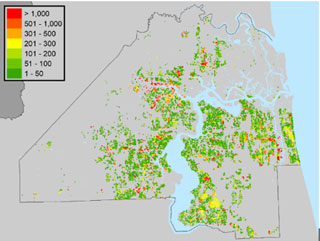

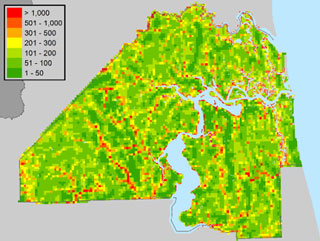

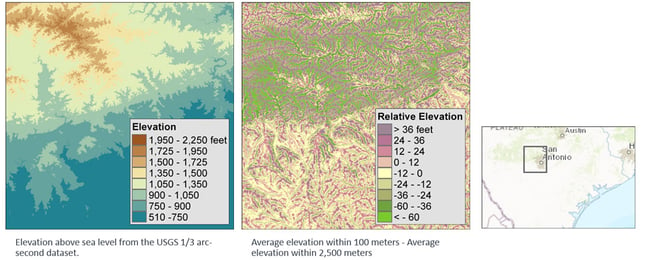

Relative elevation measures whether a point is higher or lower than the surrounding area

Rating engine

Milliman develops and maintains rating engines to calculate premiums of many existing flood programs, including the NFIP. Further, we have extensive competitive data on homeowners premiums, which can be used to assess the premium increase to policyholders of adding a flood endorsement.

Premium Rank can be used to estimate the competitiveness of a new program against likely competitors, as shown below.

Related Milliman flood insurance services

Milliman flood insurance insight

U.S. private flood insurance: The journey to build a new market

Climate gentrification and the role of flood insurance

Wading into the private insurance market

Political winds in a peak hurricane state

Four ways Hurricane Florence could ricochet across the insurance industry

What could private flood insurance look like in New Jersey and New York?

Eye of the storm: Data modelling brings new hope for flood-prone homes

Recent press

Connect with Milliman experts