はじめに

本ブリーフィングは、民間の長期介護保険(LTCI)業界の現状を調査する一連の記事の第1回目となります。本稿では、全米保険監督官協会(National Association of Insurance Commissioners、NAIC)の長期介護経験報告フォーム(Long-Term Care Experience Reporting Forms、ERFs)で、会社から提出されたデータを活用します。ERFsは2020年末の報告で大幅な修正を行ったため、本稿では、基本的に新しいデザインでも継続して入手できる情報に着目します。従来のERFsでは主に、LTCI単独契約のデータを集めることに集中していました。将来的には、このブリーフィングを拡張し、伸びているLTCIのハイブリッド契約の存在をカバーする新しいERFデザインでより多くのデータを収集していきます。本稿は、2019年のERFデータを使用しています。今後のまとめでは、2020年のERFデータを加えていく予定です。

この第1回まとめでは、被保険者数、請求金額、給付金について、単独の民間LTCI業界の全体規模に着目します。続くセクションでは、ERFsを詳細に調査し1、民間LTCIの規模、また過去10年間の変化を例示します。

Covered lives

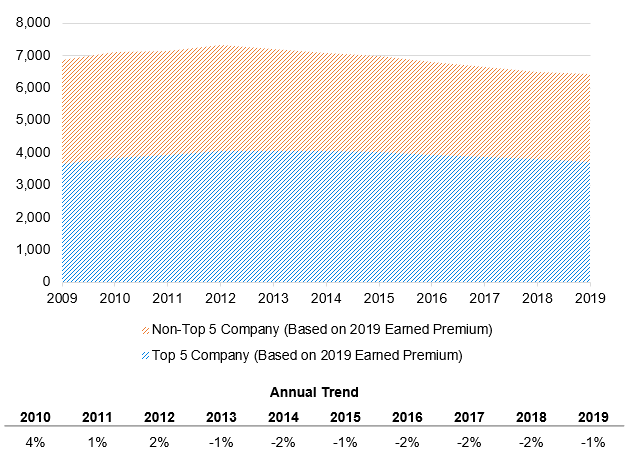

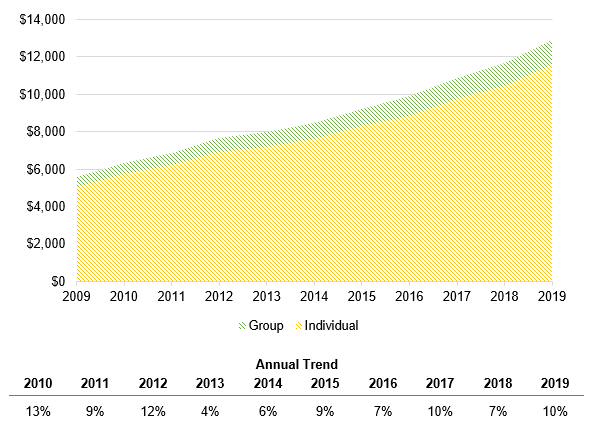

Nearly 6.5 million individuals have LTC insurance coverage through a private LTCI policy as of 2019. The number of covered lives has remained relatively steady over the last decade, but has been declining in recent years. Policy terminations have outpaced new policy issues by about 125,000 individuals per year over the last seven years, which is primarily attributable to overall declining new sales during that period. When sorting companies from high to low by earned premium in 2019, nearly 60% of all private LTCI policyholders are covered by one of the top five largest issuers (see Figure 1). The top five insurers based on 2019 in-force premium include Genworth, John Hancock, Northwestern Mutual, MetLife, and Unum.

Figure 1: Private LTCI covered lives by calendar year and company size (thousands)

Claim counts

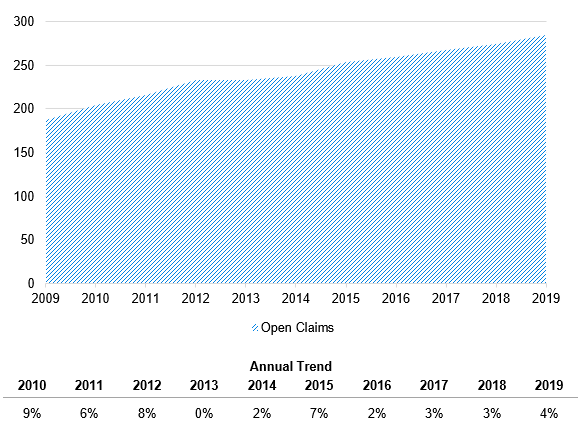

While the number of covered lives has been decreasing in recent years, a historical tally of open claims tells a different story. A net increase of 10,000 open claims per year has occurred since 2009 as policyholders age and approach the time when care is most common (see Figure 2). Over the last decade, this has accumulated to more than a 50% increase in open private LTCI claims.

Figure 2: Count of open private LTCI claims by calendar year (thousands)

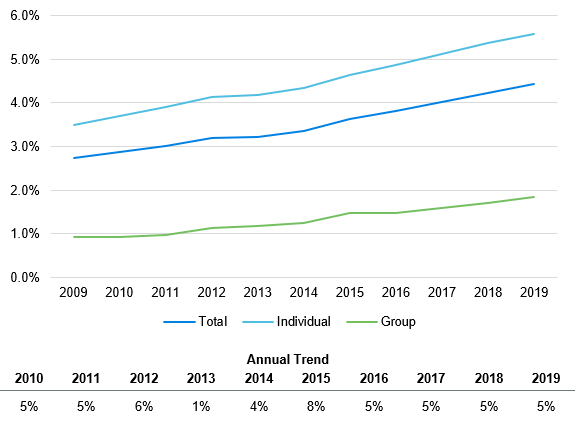

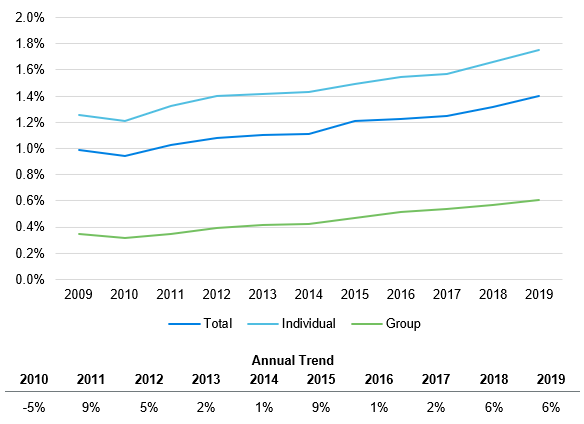

Because total policyholders covered are showing a gradual decline while open claim counts increase, prevalence (i.e., the percentage of total covered lives with an open claim) has consistently increased—see Figure 3. Similarly, incidence (i.e., the percentage of total covered lives with a new claim each year) has ticked up—see Figure 4.

When examining trends further by individual and group business, Figures 3 and 4 show prevalence and incidence are generally higher for individual business. Potential causes for this relationship include differences in insured characteristics, such as:

- Average attained age. Group business generally has lower average attained age than individual business, which could yield lower prevalence and incidence rates.

- Average policy year. Group business may have been issued more recently on average compared with individual business, which could also yield lower prevalence and incidence rates.

Figure 3: Prevalence rate by line of business, open private LTCI claims as % of covered lives

Figure 4: Incidence rate by line of business, new private LTCI claims as % of covered lives

Benefit dollars

While the growth in open claim counts certainly points to the changing size of private LTCI as a payer for LTC services, the striking growth in annual benefits incurred over the last decade underlines this point. Figure 5 illustrates this growth—a 130% cumulative increase over the last decade, reaching $12.9 billion in annual claims for 2019. Claims incurred under individual LTC plans dominate the graph, representing approximately 90% of all claim dollars in 2019. Individual LTC plans generally exhibit more claims due to a larger number of covered lives and older policyholders compared to group LTC plans.

Figure 5: Annual incurred private LTCI claims by line of business ($ millions)

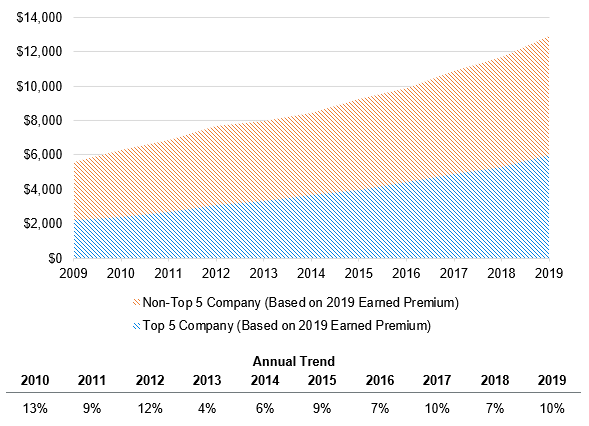

Additionally, as Figure 6 shows, more than 46% of 2019 claims are from the five largest issuers—a percentage that has been increasing over the last decade. It is worth noting, however, that these five largest insurers are also responsible for nearly 60% of covered lives (as shown in Figure 1 above).

Figure 6: Annual private LTCI claims by company size ($ millions)

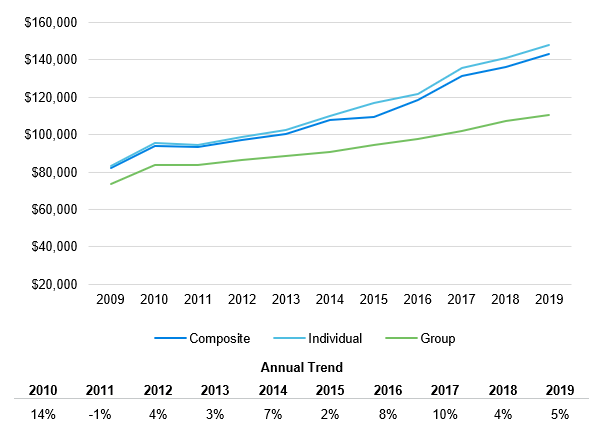

The increase in annual incurred claims is not only attributable to the growth in claimant counts, but also to the growth in the average size of claims. As seen in Figure 7, the average claim size has increased from roughly $80,000 in 2009 to $140,000 in 2019. The 5% to 6% annualized increase in average claim size likely has multiple causes, such as:

- Growing pool of money. Individuals who have a policy with inflation protection have access to a larger pool of benefits year over year.

- Increasing length of stay. Individuals may be remaining on claim and collecting benefits for a longer period than in past years.

- Rising cost of care. As the daily average cost of LTC services has increased, so has the average claim size.

Figure 7: Average private LTCI claim size by line of business

Conclusion

The need for long-term care services across the country has grown steadily over the last decade as Americans continue to age. This trend can also be clearly seen in the growth of claims in the private LTCI industry. While still a relatively small payer for long-term care services when compared to the Medicaid program, the LTCI industry is responsible for almost $13 billion in annual claims and growing and covers over six million individuals nationwide.

1All data in this article comes from company-submitted 2019 year-end NAIC Long-Term Care Experience Reporting Form 1.