ミリマンのポートフォリオマネジャーであるSimon Hoは、最近行われたセミナーでSmartShieldに寄せられたファイナンシャルアドバイザーからの質問に対応しました。その中で、SmartShieldがどのような仕組みであり、あらゆる市場環境においても投資し続けるべき説得力のある理由について解説しました。

SmartShieldは、オーストラリア市場の3,700以上のファンド管理商品の中でも独特なものです1。 投資をすることは、競争力あるリターンを生み出しつつ、リスクを直接管理するだけの一方向の賭けではないと認識しています。

研究は、リスクが運用リターンほど投資の決定に強く影響しないことを示しており2、ファイナンシャルアドバイザーはこの点についてより詳しく知っています。

COVID-19による急激な企業活動の低下により、株式市場における株価総額の約三分の一が消滅する結果となり、投資家の感情を高ぶらせ、残念な判断をする傾向が見られました。その間、株式に過剰投資していた退職者は、シーケンシングリスクにさらされたままでした。

しかし代替アプローチを取るためには、調査が必要です。ミリマンでは、アドバイザーグループを招いたフォーラムを行い、本エビデンスを検証し、SmartShieldの仕組みに関する以下の質問に答えました。

How does the risk management work?

SmartShield dynamically hedges the portfolio against volatility and extended market downturns by reserving a small portion of the portfolio to trade futures. This is the same strategy used by large insurers and institutional investors over many years to hedge their long-term liabilities.

It provides a cushion—not a guarantee—against severe downturns and ongoing volatility, making it different from products of the past. This predictable, rule-based system also preserves liquidity for investors.

"This is done systematically," says Ho. "The level of hedging is adjusted daily based on the market environment and implemented by our trading team in Sydney, Chicago, London and Amsterdam in real-time throughout the day."

The actual hedging level varies based on expected versus actual market volatility, and the level of market drawdowns. This approach provides downside protection, but also smooths returns over time.

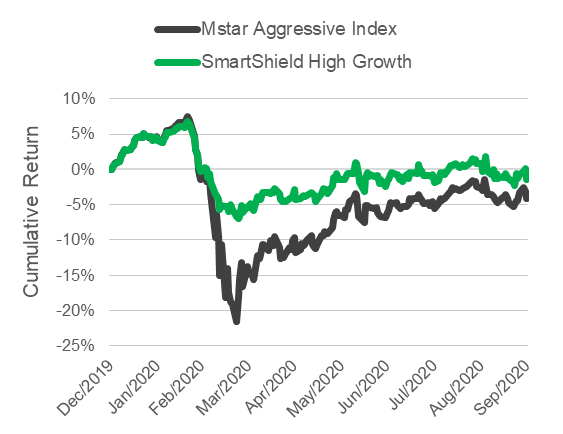

The graph in Figure 1 shows this downside protection in action (and the limits of portfolio diversification as a risk management strategy during a market crash).

Figure 1: Downside protection

Note: Prior to 3 March 2020 SmartShield performance is derived from hypothetical back-testing and actual results thereafter.

What type of assets do the SmartShield portfolios hold?

SmartShield offers four managed account portfolios: Moderate, Balanced, Growth and High Growth. The strategic asset allocation of each fund is based on the Morningstar Multi-Sector Market Indices3—with one important difference.

"We allocate roughly 10% more growth assets compared to the benchmark," Ho says.

"This is to recognise the fact that we can dial up and down the equity exposure as part of our risk management process through trading futures. This gives the portfolio extra power during benign periods, knowing that in volatile times we can hedge the equity exposure rather quickly as we have demonstrated during COVID-19."

This extra allocation to growth assets has been fine-tuned to offset hedging costs over the long term and maintain performance when markets are slowly trending up over an extended period.

How are the fees kept so low?

Historically, many funds management products that offer some form of protection came with high fees. SmartShield is a different type of product, offering downside protection through futures, which are highly liquid and are expected to cost less than similar option strategies.

"If you were to buy a put option on the market, it is expected to cost more over the long run, partly because you're buying it through an investment bank which may need to cover their capital charges and profit margins," says Ho.

Milliman also has significant global trading infrastructure in place because it implements these strategies across more than USD 50 billion in assets for global asset owners.

"Due to our sheer economies of scale, we're able to offer low-cost risk management solutions to retail clients," Ho says.

The underlying investments in each portfolio are inherently low-cost because they are invested in exchange-traded funds offered by Vanguard, iShares and BetaShares. This keeps the products very competitively priced with the total investment costs sitting below 50 basis points.

What type of returns should investors expect?

The SmartShield portfolios aim to deliver investment returns that are similar to their benchmark, the Morningstar Multi-Sector Indices. However, the downside protection makes the SmartShield risk profiles of managed account portfolios different.

"Volatility will be a lot more subdued," Ho says.

In fact, the volatility of the SmartShield portfolios was approximately one-third of the volatility of their respective Morningstar multi-sector indices during the COVID-19 downturn. This clearly demonstrates the effectiveness of the downside protection.

The hedging strategy can produce a drag on performance during positive markets, but this is partly offset by the extra 10% allocation to growth assets.

How can an adviser best use SmartShield?

While SmartShield is primarily targeted toward pre-retirees and retirees, it offers a solution for many different types of investors:

- Retirees or those approaching retirement who are exposed to sequencing risk

- Risk-averse investors who may withdraw their money at a low point in the market

- Investors who would prefer not to ride out a potential long market downturn

Ho says SmartShield's downside protection and lower volatility means advisers don't have to try to time their market calls, which is notoriously difficult to do.

"A lot of advisers' clients have their assets in cash-like assets," he says. "It's quite tiring to keep having conversations with investors about when we are going to move that 'dry powder' into growth assets again. SmartShield takes a lot of the guesswork out of the adviser's hands."

Trying to time the market often means missing out on a market recovery. The upswing after COVID-19 was one of the fastest in history, meaning many investors who had moved to cash actually missed out.

SmartShield offers a genuine solution for investors who need the potentially higher returns of growth assets yet can't accept the higher risk that comes with it.

You can check the potential benefits of downside protection on your client portfolios at https://advice.milliman.com/en/insight/The-SmartShield-digital-portfolio-simulator.

For more information about Milliman go to https://au.milliman.com/en/

FOR INVESTMENT PROFESSIONAL USE ONLY

Milliman Pty Ltd ABN 51 093 828 418 AFSL 340679 (Milliman AU) for provision to Australian financial services (AFS) licensees and their representatives (and for other persons who are wholesale clients under section 761G of the Corporations Act). Not for public use or distribution. Past performance is not indicative of future results. Recipients must make their own independent decisions regarding any strategies or securities or financial instruments mentioned herein. Milliman does not make any representations that products or services described or referenced herein are suitable or appropriate for the recipient. Many of the products and services described or referenced herein involve significant risks, and the recipient should not make any decision or enter into any transaction unless the recipient has fully understood all such risks and has independently determined that such decisions or transactions are appropriate for the recipient. Any discussion of risks contained herein with respect to any product or service should not be considered to be a disclosure of all risks or a complete discussion of the risks involved. The recipient should not construe any of the material contained herein as investment, hedging, trading, legal, regulatory, tax, accounting or other advice. The recipient should not act on any information in this document without consulting its investment, hedging, trading, legal, regulatory, tax, accounting and other advisers. Milliman does not ensure a profit or guarantee against loss. Materials may not be reproduced without the express consent of Milliman.

1Australian Securities and Investments Commission. Review of competition in the Australian funds management industry. Retrieved 8 July 2021 from https://asic.gov.au/regulatory-resources/funds-management/review-of-competition-in-the-australian-funds-management-industry.

2High historical returns are a strong determinant of investment allocation decisions, while risk factors are not strong influences on investment decisions, according to a study that looked at net cash flows data from 1991 to 2013. See Gupta, Rakesh & Jithendranathan, Thadavillil (March 2012). Fund flows and past performance in Australian managed funds. Accounting Research Journal 131. Retrieved 8 July 2021 from https://www.researchgate.net/publication/236165375_Fund_flows_and_past_performance_in_Australian_managed_funds.

3See https://www.morningstar.com/content/dam/marketing/apac/au/pdfs/Legal/MultiSector_IndicesAU_2018-06.pdf.