課題

あるお客様がその確定給付型年金プランについて積立拠出のボラティリティーと投資関連費用を管理する方法を求めていました。

The solution

Evaluating the current plan’s assets

After reviewing the asset information, we determined that it was based on a model provided by the prior advisor, allocated 60% to equity and 40% to fixed income. In discussions with the client, it was noted that there had been no analysis of the plan’s liabilities in developing the prior asset allocation. However, the prior allocation was found to be nearly optimal from a risk and return perspective with regard to the assets. What was missing was a connection of the assets to the liabilities.

In reviewing individual plan investment managers, we found that the plan had eight actively-managed mutual funds from the same investment manager and trust company which provided custodial and benefit payment services for the plan. The total investment management expense for the plan was approximately 0.91%.

Through this preliminary investment review, we concluded that investment management expenses could be reduced significantly by using Milliman’s Alpha-Beta liability-driven investment strategy. For an Alpha-Beta portfolio, Milliman pairs broad-based index (“Beta”) exposure to major, efficient asset classes, with active management (“Alpha”) in specialty classes in an attempt to lessen volatility and enhance returns.

Analyzing the structure of plan liabilities

What is LDI?

An LDI strategy attempts to match the duration of plan liabilities with fixed income investments that have a similar duration. As interest rates shift, liabilities and assets move in an inverse direction. For example, if interest rates decline 1%, the value of liabilities with a duration of 10 years will increase by 10%. Hence, if a bond portfolio with a duration of 10 years experiences a 1% interest rate decline, the value will increase by 10%. As you can see in this simple scenario, the negative impact to liabilities would be offset by the positive impact to the investment portfolio, a fully synchronized asset liability portfolio.

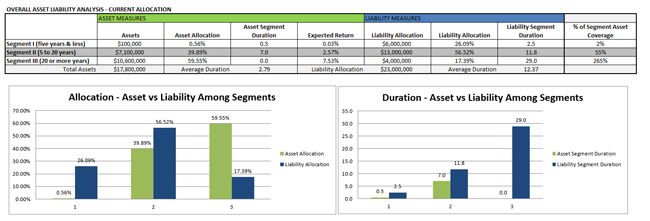

In assessing the structure of plan liabilities to assets, the client wanted to see if the two could be more closely linked, reducing the variability of the contributions as well as the funded status. Therefore, we examined the implementation of a liability-driven investment strategy (LDI), looking at the current allocation and reconciling it to the duration of plan liabilities from the plan’s actuarial valuation output, to assess the variability of funded status as interest rates will affect the value of liabilities from an actuarial perspective and fixed income assets from an investment perspective.

Utilizing Pension Protection Act (PPA) segments, in Exhibit 1, Milliman categorized the allocation and duration of plan liabilities into three different segments: short (five years and less), intermediate (five to 20 years), and long (20 or more years) and compared that to the allocation and duration of the underlying investments.

We found that there was essentially no coverage of plan assets to short-term liabilities as well as mismatches in the other segments of liabilities, an aspect that would be addressed in developing the future glide path allocation for the plan. The glide path is a discipline that moves more assets into LDI as the plan becomes better funded. Based on the funding level of the plan, it was also determined that the moderate growth structure of assets (60/40) mix was generally reasonable and would be considered in the future allocation for the plan’s assets.

Based on the analysis of plan liabilities, we determined that some asset categories should be added to provide more diversification and allow the fixed income portion of the portfolio to be allocated to partially match the duration of plan liabilities. In particular, for fixed income, the committee considered adding inflation-linked, short-term, investment-grade and long-term fixed income. For equities, the committee considered adding mid-cap U.S. equity, emerging markets equity, and real estate to better diversify the plan and enhance its expected return.

Forming the asset-liability investment strategy

In developing the asset allocation, the client’s overall goal was to reduce funded status volatility while generating positive returns over time to improve the plan’s funded status.

A detailed report was provided to the client with illustrations of various asset allocation scenarios, summarizing the current structure of plan assets and liabilities as well as levels of expected return and risk (volatility) for each allocation scenario. The client, now understanding the potential impact of asset and funded status volatility, selected an allocation that would provide a level of return and volatility in line with their goals.

The allocation essentially maintained the mix between equity and fixed income, but reallocated the fixed income in a manner that better synchronized shorter-term fixed income to shorter-term liabilities. This is the first step along a glide path to a full LDI strategy as the plan’s funded status improves.

Implementation of the strategy

In assessing the current mix of actively managed funds, we found that implementing the Alpha-Beta investment strategy provided the plan with broader diversification opportunities across efficient asset classes while reducing overall plan expenses. The mapping strategy reallocated the plan to a series of new investment managers, selecting certain asset categories where index funds were utilized and other categories where active managers were used. In implementing the investment portfolio, a number of managers were added, some index managers replaced active managers, and the overall effect was reducing investment management expenses by 0.70%, from 0.91% for their prior portfolio of managers to 0.21% for the new portfolio.

Formalizing the investment policy

To formalize their approved actions, Milliman drafted an investment policy statement (IPS) for the investment committee to review, approve, and sign. The IPS stated roles and responsibilities of the board, committee, and Milliman as well as the investment strategy and methods for monitoring managers. In addition, it included an asset allocation glide path to follow, defining target allocation changes to be made as funded status improves, leading to a full LDI strategy as the plan reaches fully funded status.

Outcome

In working with Milliman, the client was able to gain a better understanding of the relationship between plan assets and plan liabilities in managing their pension plan’s funded status. By implementing the Alpha-Beta asset-liability investment strategy, the client will reduce investment management expenses, achieve broader asset class diversification, and have a defined path for the future management of their pension plan.