オーストラリアの年金業界の2兆3000億豪ドルの多くをベビーブーマーが占めていますが、若いミレニアル世代も急速にその資産を増やしています。

Roy Morgan Research によると、年金ファンド残高における若い世代のシェアは、2017年9月末までの10年間に(6.4%から14.6%へと)倍以上になりました。一方、多くのベビーブーマーがこの10年間に貯蓄を引き出したため、そのシェアは12.1%減少しました。

しかし、ミレニアル世代は上昇傾向にあるものの、まだ数十年にわたって成果を活用できない人たちに年金給付商品を販売することは、退職が近づいている高齢の加入者に販売するよりもはるかに難しいものです。

Baby Boomers dominate Australia’s $2.3 trillion superannuation industry, but younger Millennials are catching up fast.

Their share of superannuation fund balances more than doubled over the decade ended September 2017 (from 6.4% to 14.6%), according to Roy Morgan Research. Baby Boomers share declined by 12.1 percentage points as many drew down on their savings over the decade.

But while Millennials are on the rise, trying to sell the benefits of a product to those who won’t reap the rewards for decades is a far more difficult task than for older members nearing retirement.

While each fund has its own strategies, they all need digital tools powered by accurate big data if they are to truly engage the growing Millennial market. If they fail to do so, funds will see significant losses as younger members switch funds, often in the 30-40 year age bracket.

Each generation may be subtly different than the last (although perhaps not as radically different as some suggest given that memories of youth fade with experience), but what is not in doubt is that new technology, powered by the interconnected nature of the internet, has become a crucial component of our lives and member expectations.

This is second nature to younger members–and many are not impressed.

Millennials rated their satisfaction about a full third lower than Baby Boomers, suggesting low levels of engagement and brand loyalty, according to Roy Morgan.

The industry has long grappled with significant outflows directed towards self-managed super funds and has, more recently, been surprised by the rise of technology and youth-focused funds such as GROW Super.

Use data to understand and drive engagement with younger members

Milliman’s Retirement Expenditures and Spending Profiles (ESP) service has revealed the behaviour and trends of older investors by tracking the real-world behaviour of more than 300,000 retirees using bank transactions, retail spending and property data.

Equally, that data can be applied to the broader population and reveal much about the expenditures of younger people as shown in the following graph.

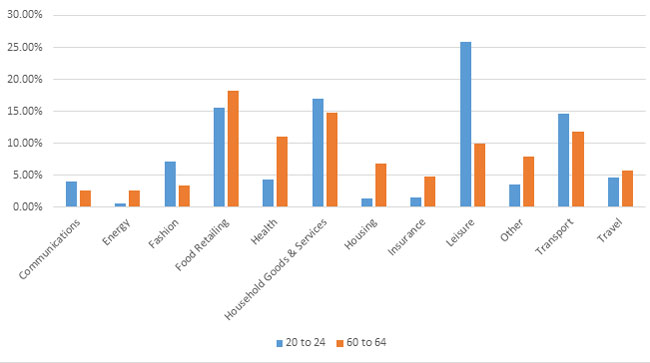

Figure 1: Expenditure - young versus mature

Source: Milliman Retirement Expectations and Spending Profiles data

It shows that spend on leisure as a percentage of the household budget peaks between ages 20-24 (although it peaks in dollar terms between ages 35-39). Older Australians spend far less on leisure, although these figures also vary substantially for individual households depending on other factors, including where retirees live.

Housing expenditure starts at just 1.38% for 20-24-year-olds and rises over the years as they buy homes or move into larger residences. Health costs follow an inverse pattern, starting low for 20-24-year-olds (4.25%) and steadily rising through the years, approaching 12% into retirement.

These expenditure decisions are being made against a more challenging economic environment for younger members.

Financial support from the government to attend university has been slashed, while other government payments are also under pressure. Wage growth has remained heavily subdued a decade after the global financial crisis, and the rise of the gig economy is eroding many traditional employment safeguards. Gaining a foothold in the housing market is becoming more challenging along the populous east coast where property prices have soared.

Where does super fit? It is a product that young people are forced to buy via the superannuation guarantee, partly because the benefits are heavily discounted given they are set well into the future.

Yet the overwhelming message many younger members often receive from the media is that their contributions are not high enough and that they’re unlikely to have enough to retire in comfort. Given the priorities and pressures on Millennials, this is likely to cause total disengagement.

Meanwhile, contrary to conventional expectations, there is some evidence that young investors may be more risk averse than older investors. Four in five young investors said they preferred guaranteed or stable investment returns, according to the ASX Australian Investor Survey 2017. It could be a sign of the GFC’s impact during formative years or perhaps lower financial knowledge and experience.

It will take a more subtle range of communication that engages the values, priorities and interests of Millennials. Each fund will develop its own suite of services, but they will only be as good as the research which underpins them.

In this manner, funds can demonstrate their true value and build engagement with members through their entire lives and into retirement.

Disclaimers

This document has been prepared by Milliman Pty Ltd ABN 51 093 828 418 AFSL 340679 (Milliman AU) for provision to Australian financial services (AFS) licensees and their representatives, and for other persons who are wholesale clients under section 761G of the Corporations Act.

To the extent that this document may contain financial product advice, it is general advice only as it does not take into account the objectives, financial situation or needs of any particular person. Further, any such general advice does not relate to any particular financial product and is not intended to influence any person in making a decision in relation to a particular financial product. No remuneration (including a commission) or other benefit is received by Milliman AU or its associates in relation to any advice in this document apart from that which it would receive without giving such advice. No recommendation, opinion, offer, solicitation or advertisement to buy or sell any financial products or acquire any services of the type referred to or to adopt any particular investment strategy is made in this document to any person.

The information in relation to the types of financial products or services referred to in this document reflects the opinions of Milliman AU at the time the information is prepared and may not be representative of the views of Milliman, Inc., Milliman Financial Risk Management LLC, or any other company in the Milliman group (Milliman group). If AFS licensees or their representatives give any advice to their clients based on the information in this document they must take full responsibility for that advice having satisfied themselves as to the accuracy of the information and opinions expressed and must not expressly or impliedly attribute the advice or any part of it to Milliman AU or any other company in the Milliman group. Further, any person making an investment decision taking into account the information in this document must satisfy themselves as to the accuracy of the information and opinions expressed. Many of the types of products and services described or referred to in this document involve significant risks and may not be suitable for all investors. No advice in relation to products or services of the type referred to should be given or any decision made or transaction entered into based on the information in this document. Any disclosure document for particular financial products should be obtained from the provider of those products and read and all relevant risks must be fully understood and an independent determination made, after obtaining any required professional advice, that such financial products, services or transactions are appropriate having regard to the investor's objectives, financial situation or needs.

All investment involves risks. Any discussion of risks contained in this document with respect to any type of product or service should not be considered to be a disclosure of all risks or a complete discussion of the risks involved.

Past performance information provided in this document is not indicative of future results and the illustrations are not intended to project or predict future investment returns.