ギャップイベントは、実際に起こることは稀ですが、煩わしい現象です。

Brexitを決めた投票はその典型的事例です。2016年6月、英国人が予想に反してEU脱退を選択した際、主要株式市場の一部では複数市場の取引時間をまたいで下落しました。投資家が翌朝起きてみると、株価は急落していました。

その後大部分の株価は数日のうちに急速に回復しましたが、その他の歴史的なギャップイベントは一層予測が困難で、数期にわたり高いボラティリティーとなり、一層の株価下落につながりました。

S&P 500は、2017年7月までの50年間における34のギャップイベント(日中最安値と前日終値の差が5%超と定義)を提示しました。これによると、取引日の0.27%が該当したのに過ぎませんが、1987年10月20日の一日で25%近い下落など、忘れられないギャップイベントもあります。

ほとんどの取引所が今では、こうした規模の下落を回避するための売買停止措置を導入していますが、いずれにしても日中突然5%超下落する可能性は投資家によってはリスク許容度を超えます。

課題:高コストとタイミングの難しさ

プットオプションを用いてギャップリスクに備える投資家は、大きな課題に直面します。継続的なプロテクションを維持するには、費用が高く、時期を決めるのが難しく、効果を生まないこともあります。

一方で、プットのスプレッドおよびディープ・アウトオブザマネー・オプションを購入しても、多くのポートフォリオは大幅にギャップイベントに晒されたままです。

例えば、10%のギャップイベントを考えてみます。ある投資家が3か月の97%/90%プットスプレッドを最高値で1.5%の手数料(年間維持費6%)で購入したとします。この戦略では、ポートフォリオは満了時に市場の下落に対して45%参加をした状態のままです。1

一方ギャップイベントが20%の場合、この戦略では、ポートフォリオは満期時に下落に対して72.5%のエクスポージャーを残しています(どちらもストライクは最高値からを想定)。2

瞬間的なギャッププロテクションの水準は、非常に変動しやすく、オプションがストライクされるポイントと残りの期間に大きく依存します。

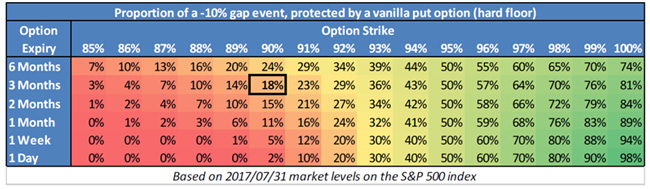

「ハードフロア」型のオプション・ストラクチャーは、役立つものの高価になります。以下の表は、単純化したヴァニラ・プットオプション(「ハードフロア」を表す時価評価)と-10%のギャップイベントに対するプロテクションの水準を示しています。プロテクションの水準は、ストライクの水準と満期までの残存期間を含む複数の要因で決定されることをハイライトしています。

例えば、3か月の90%プットオプションの保有は、想定元本に対して1.8%のリターン、もしくはギャップイベントに対して単に18%のプロテクションを生みます(オプションの想定元本は基になる保有額と等しいとした場合)。オプションが満期を迎えるにつれて市場が下がる傾向の場合、ハードフロアが利益を生みます。一方、市場はこれまでも大きな下落の後で急速に回復しています。

物理的なオプションを用いたリスク管理戦略の中で、オプション・ストライクの水準は、通常、時間によって任意に決まります。(スプレッドおよびアウトライトの購入における)ストライクの水準の任意の性質は、プロテクションの水準に関する不確実性を加えます。

Brexit関連売りに対する5月末のポートフォリオ価値をプロテクトする目的の米国、英国、ユーロ圏の仮想の投資家3人を分析することで、プットオプションによる高コストとタイミングの難しさを 既に示しました。

マネージド・リスク:代替戦略の評価

オプション、スワップ、スワプションは、利益をもたらしますが同時に課題ももたらします。継続的なオプション・プロテクション戦略は、効率性はそれほど高くなく、ダイナミックヘッジ戦略以上には必ずしもポートフォリオを保護しません。

Milliman Managed Risk Strategy™(MMRS)は、キャッシュ・バッファーを有し、ヘッジ資産(典型的に上場先物契約)を使用して、市場混乱期の資本を保護し、ボラティリティーを管理します。

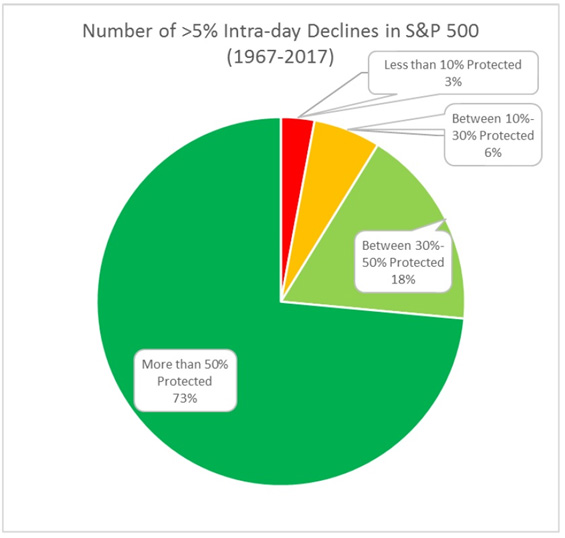

これは、本戦略がギャップイベントに対して常に何らかのプロテクションを提供することを目指していることを意味します。以下のチャートは、同じ50年の間でS&P 500ポートフォリオに適用されたリスク管理戦略が提供するプロテクションの水準を示しています。これは、73%を超える期間において、ポートフォリオの50%以上に対するプロテクションを提供していたことになります。

ギャップイベントは典型的に、ボラティリティーの高い期間にストライクとなるか、市場の下落を持ちこたえるため、この比較的高い水準のプロテクションが行われます。これはつまり、ボラティリティー管理およびリスク管理された戦略が、最高水準のプロテクションを提供した時です。

これは、オプションベース戦略ではエクスポージャーを残しうる市場の状態の定性的評価に基づく裁量的決定ではなく、定量的市場データに対するあらかじめ規定されたルールベースの対応です。

またミリマンは、(該当する)多くの主要先物取引所で可能となっている夜間取引を含め、全ての主要な市場をカバーする3拠点のトレーディングデスクの連携とほとんどの主要ブローカーとの継続的コンタクトにより、ギャップイベントが発生しうる期間を最小化します。これにより、ミリマンのトレーダーは、ギャップイベントの発生後に気付くのではなく、マーケットイベントが発生した際の迅速かつ適切な対応が可能になります。

ギャップリスクに対してポートフォリオを保護するための単純な解はありませんが、目の前にある戦略を注意深く評価することが、最も効率的で費用効果の高いアプローチを確かなものにするはずです。

デリバティブ戦略に関するさらに詳しい情報は、ミリマン東京オフィス([email protected])までお問い合わせください。

197%/90%のプットスプレッドでは、97%のロングストライクが3%の確率でポートフォリオをアウトオブザマネーにします。これは、ポートフォリオが1.5%の費用で10%の市場の下落に4.5%参加することを意味し、市場の下落に45%参加していることと等しくなります。

297%/90%のプットスプレッドでは、97%のロングストライクが3%の確率でポートフォリオをアウトオブザマネーにし、プロテクションを90%のショートストライクの水準に限定します。これは、投資家が1.5%の費用で10%の市場の最初の下落に4.5%参加し、さらなる10%の下落に全面的に参加していることとなります。これは、ポートフォリオが20%の市場の下落に14.5%参加していることを意味し、市場の下落に72.5%参加していることと等しくなります。

ディスクレーマー

本稿は、Milliman Pty Ltd ABN 51 093 828 418 AFSL 340679(Milliman AU)がオーストラリア金融サービス(Australian financial services、AFS)免許業者およびその代表者(さらに法人法(Corporations Act)セクション761Gにおける卸売顧客であるそれ以外の方)向けに作成しました。

これらの結果は、特定の制約を内在するシミュレーション結果もしくは仮想のパフォーマンス結果に基づいています。実際のパフォーマンスによる結果とは異なり、これらの結果は実際の取引を表すものではありません。またこれらの取引は実際に執行されていないため、これらの結果は、該当する場合、流動性の欠如など特定の市場要因の影響を過小または過大に相殺している場合があります。また一般にシミュレーションや仮想のトレーディング・プログラムは、後知恵で設計されたという事実があります。アカウントがここに示したものと同様の利益または損失を達成するあるいは達成しそうであることを表明するものではありません。ミリマンは、基になるファンドの管理をしていません。

本稿では対象や特定の人物の財務状態またはニーズを考慮していないため、金融商品の助言を含んでいる可能性があるという範囲において、これは一般的助言としてとらえるものです。さらにこうした一般的助言は、いかなる特定の金融商品に関連するものでもなく、特定の金融商品に関する決定を行うに当たりいかなる人物に対しても影響を与えることを意図していません。また、Milliman AUおよびその従業員は、本稿における助言をしなくても受けたであろうものを除き、本稿における助言に関連して(手数料を含む)いかなる報酬も利益も受けていません。本稿では、いかなる人物に対しても、いかなる金融商品の売買、参照された種類のサービスの獲得、特定の投資戦略の採用について、何ら推奨、意見、提供、勧誘、広告をするものではありません。

本稿に参照された種類の金融商品やサービスに関する情報は、本情報を作成した時点でのMilliman AUの意見を反映しており、Milliman, Inc.、Milliman Financial Risk Management LLC、その他ミリマンのグループ傘下の法人(ミリマングループ)の見解を表すものでない場合があります。AFS免許業者やその代表者が本稿にある情報に基づいた助言を顧客に対して行う場合、当該情報の正確性や表明する意見に関して自身で全責任を負わなくてはなりません。また、明示的・暗示的にその助言や助言の一部をMilliman AUおよび他のミリマングループ傘下の法人に起因させてはなりません。さらに、本稿にある情報を考慮して投資に関わる決断をする際は必ず、その情報の正確性および表明された意見に自身が納得していなくてはなりません。本稿に記載もしくは参照された種類の商品およびサービスの多くは重大なリスクを伴い、全ての投資家にふさわしいわけではありません。参照された種類の商品やサービスに関するなんらかの助言と考えるべきではなく、また、本稿にある情報に基づいていかなる決定や取引の実施をすべきではありません。特定の金融商品に関するあらゆる開示文書は、係る商品のプロバイダーから入手して確認し、全ての関係するリスクを完全に理解し、係る金融商品、サービス、取引は、投資家の目的、財務状況、ニーズに鑑み、適切であるかどうか必要となる専門家の助言を得た上で独立した決定を行わなくてはなりません。

あらゆる投資にリスクが伴います。本稿における何らかの種類の商品やサービスに関わるリスクの議論は、関係するすべてのリスクの開示やその完全な説明と考えてはなりません。