Super Typhoon Haiyan stands to rewrite the record books as the costliest natural catastrophe in the history of the Philippines. One of the strongest tropical cyclones to make landfall on record, Haiyan is estimated to have dealt between US$6.5 billion and US$14.5 billion in economic damage to the Philippines, equaling up to 5.5% of the country’s GDP.1 While the Philippines is a frequent victim of tropical cyclone strikes, few storms have hit the island with such force and destructive capability.

Despite recent growth, insurance markets remain underdeveloped in emerging Asian economies such as the Philippines. As a result, the governments of these countries rely on a range of alternative funding strategies to support disaster recovery and reconstruction efforts. However, most common strategies are usually insufficient to deal with a catastrophe of Haiyan’s size. Thus, over the last several years, developing Asian nations have begun to explore insurance-based sovereign risk transfer mechanisms as a way of securing additional catastrophe protection for their populations.

Although few of these initiatives have progressed past the planning stage to date, the prognosis for growth is good. Insurance capital is increasingly turning to Asia as a source of growth and diversifying perils. Additionally, the international development community has already partnered with a number of emerging economies to launch innovative risk-transfer structures such as catastrophe risk pools and sovereign catastrophe bonds (cat bonds).

Thus, while Haiyan was not a major insurance event, its effects should drive continued interest in sovereign catastrophe risk transfer products—increasing the odds that today’s emerging economies will be able to rely on global insurance markets to help fund future Haiyans.

Effects of the ex-post funding approach to disaster recovery

Historically, governments in developing countries have preferred ex-post disaster financing techniques—those that require little to no investment prior to the disaster. The reasons for this are both social and political: Investments that produce a visible benefit today are more popular than those that promise contingent benefits should a once-in-a-lifetime catastrophe occur.

Ex-post funding techniques may be adequate to finance recoveries from moderate-sized catastrophes. However, as shown below, such techniques have serious limitations when confronted with “the big one.”

Reallocation of government expenditures

For the reasons mentioned above, most developing nations do not build up substantial government disaster funds. At best, some catastrophe-prone countries (like the Philippines) may anticipate a certain level of government expense toward rebuilding in a given year.

Once these planned expenditures are exhausted, recovery efforts can still be financed internally by reallocating funds from other government projects. However, these disaster reallocations frequently impede the future development of the country’s economy. Each dollar devoted to disaster relief becomes a dollar taken away from infrastructure projects, education, or other key investments.

Thus, emerging economies generally have a limited ability to effectively self-finance severe disaster losses. The “Calamity Fund” of the Philippine National Government (PNG) is allocated approximately US$170 million per year in the national budget.2 If the current estimates of up to US$14.5 billion in total economic loss and up to US$700 million in insured loss are accurate,3 the uninsured losses from Haiyan—after swamping the Calamity Fund—will exceed 25% of the PNG’s total budget for 2014.4 Finding external funding sources will be an economic and political necessity.

Dedicated disaster relief loans from the international community

Concessional disaster relief loans from international development banks are a major source of catastrophe funds for emerging economies. One of the most prominent disaster loans is the World Bank’s Catastrophe Deferred Drawdown Option (CAT DDO). The CAT DDO offers countries a loan equal to the lesser of US$500 million or 0.25% of a country’s GDP at below-market interest rates. These loans are designed to fill the immediate liquidity need that occurs during the crucial first weeks of the recovery effort.

In 2011, the Philippines received a CAT DDO loan of US$500 million to fund recovery efforts related to Cyclone Washi.5 The entire balance of this loan was still outstanding when Haiyan hit, making the Philippines technically ineligible for further CAT DDO funds. Nevertheless, the World Bank still approved further emergency loans related to Haiyan of US$500 million, matching another US$500 million loan offered by the Asian Development Bank.6

After a typical natural catastrophe, such loans might represent the key piece of disaster funding. However, these loans may end up covering less than 10% of the uninsured losses from Haiyan. In addition, they contribute to the continuing buildup of foreign debt on the Philippines' balance sheet.

Donations and other forms of aid from foreign countries

The amount of international aid received after a natural catastrophe depends heavily on the amount of the event’s coverage in the global media. Scenes of Haiyan’s aftermath have captured widespread attention, resulting in pledges of disaster aid from the international community in the form of essential supplies, skilled personnel, and financial donations.

However, foreign aid—despite the press it receives—almost always accounts for a relatively small portion of the disaster relief effort. Based on history, it is likely that only 10% to 15% of the total damages from Haiyan will eventually be covered by foreign aid. In addition, foreign aid can sometimes take months to arrive on the scene post-catastrophe, and is frequently restricted to projects of the donor’s choosing.7

Addressing the funding gap after severe tail events

Even after exhausting the usual ex-post sources, the governments of developing countries face significant funding gaps after the worst catastrophes. Without the existence of proper mitigation and recovery mechanisms, these events are likely to lead to economic stress and even political instability (e.g., Haiti after the 2010 earthquake). As a result, several emerging economies have begun to explore the potential of using ex-ante sovereign risk transfer techniques such as catastrophe risk pools and catastrophe (cat) bonds to provide an additional layer of protection.

Domestic and regional catastrophe risk pools

Governments can strengthen local catastrophe insurance markets by creating domestic catastrophe risk pools. An example in the developing world is Thailand's National Catastrophe Insurance Fund (NCIF), created in response to the devastating Thai Floods of 2011.8 In these pools, the government often serves as a reinsurer, providing (often mandatory) coverage to any insurer writing exposures in the country. These arrangements provide an important source of diversification and risk pooling, but are reliant on the primary market to write policies for the government to reinsure.

In other instances, small developing countries have coordinated to create a regional catastrophe risk pool comprised of several nations. These pools are frequently organized and partially capitalized by the international development community. They allow countries to spread catastrophe risk across a wide geographic region (as opposed to domestic pools, which cover only a single country), and offer consolidated access to the global reinsurance market. Pools also fund educational initiatives and invest in regional loss mitigation projects.

The two most prominent pools to date are the Caribbean Catastrophe Risk Insurance Facility (CCRIF) and the Pacific Catastrophe Risk Insurance Pilot (PCRIP). Each was founded with the cooperation (and funding assistance) of the World Bank. These two pools are also similar in other ways: Both are comprised of small island nations with high disaster vulnerability, both have enabled their members to obtain catastrophe reinsurance coverage at competitive rates, and both have proven popular among members (as evidenced by high annual renewal rates).

Insurance-linked securities

Another alternative is the use of insurance-linked securities such as cat bonds to transfer catastrophe risk directly to global financial markets. International development banks have championed the potential for emerging economies of solutions based on insurance-linked securities (ILS),9,10 and several individual countries, including Taiwan11 and the Philippines,12 have recently expressed interest in sovereign cat bond transactions.

For both risk pools and cat bonds, the use of parametric triggers, which base payouts on the physical characteristics of natural catastrophes, is almost inevitable in developing countries, which is due to difficulties in assessing actual insured loss after a disaster. Although parametric triggers do have downsides (namely, the introduction of basis risk), their simplicity provides a counterbalancing benefit to emerging market sponsors. Similar to disaster relief loans, insurance mechanisms based on parametric triggers can provide funding during the critical first weeks post-catastrophe, when the humanitarian need is highest.

Insurance-based catastrophe risk transfer: Challenges and trends

Insurance capital (defined here to include ILS investors in the financial markets) has anticipated Asia’s role as a driver of future growth and has already made inroads into developed Asian markets such as Japan. The use of insurance-based sovereign risk transfer mechanisms in the developing world seems like a natural next step. Nevertheless, it has faced several challenges to date.

Historically, there has been almost no demand for ILS products among the governments of developing countries, which is due to their cost and complexity. However, there are signs that this demand is now starting to rise. Understanding of insurance products has grown as disaster preparation has become a key political topic for developing nations (particularly regarding the potential effects of climate change).

Further, investors may be hesitant to invest in sovereign ILS because of the relationship risks associated with government turnover. Today’s government leaders may not be in office next year, and next year’s leaders might not place a high priority on maintaining existing insurance arrangements. This risk can be partially mitigated either by funneling risk through regional organizations (such as catastrophe risk pools) or by locking in multiyear deals (such as cat bonds).

Additionally, the costs of issuing an insurance-based product are significantly higher in the Asia-Pacific region, which is due to a lack of refined catastrophe data and models. These shortcomings dramatically increase the uncertainty of the models’ output, which in turn increases the cost of coverage.

Finally, insurance-based solutions typically involve significant startup costs that are frequently beyond the budgets of developing nations. Risk pools require initial capitalization, and cat bonds require up-front structuring costs such as registering a special-purpose vehicle and marketing the security.

However, two trends are helping to erode these barriers. First, the catastrophe reinsurance market has seen a dramatic increase in interest over the past year from nontraditional market participants such as hedge funds, pension funds, and other institutional investors. Unprecedented amounts of this “alternative capital” have begun to invest in the market, resulting in a drop in the price of catastrophe risk protection. As competition for “peak risks” such as U.S. hurricane and Japanese earthquake becomes increasingly fierce, investors are likely to look to new products and markets to sustain high returns.

Equally as important, the international development community has become increasingly proficient at organizing joint public-private initiatives for insuring catastrophe risk. The World Bank in particular was a driving force behind Mexico’s MultiCat cat bond offering and the formation of the CCRIF and PCRIP. The availability of donor funds and expertise provides a significant incentive for developing nations to pursue sovereign risk transfer initiatives.

Case study: The post-Haiyan Philippines

Although it is too late for insurance-based risk transfer mechanisms to help finance the Philippines’ recovery from Haiyan, it is worth reviewing the considerations a post-Haiyan Philippines might face in trying to transfer catastrophe risk in the current marketplace.

A regional risk pool would provide long-term risk transfer, but has sizable startup costs and requires international cooperation.

One option would be for the Philippines to develop a government-funded domestic catastrophic risk pool similar to Thailand's NCIF. Unfortunately, the Philippines' low rate of non-life insurance penetration limits the utility of a government reinsurance pool that depends on policies written by primary insurers. This low amount of coverage is notable even among developing nations: For comparison, Thailand has non-life insurance coverage that is over four times higher than that of the Philippines (measured as a percentage of GDP).13

Another option would be for the Philippines to join other developing nations in Southeast Asia in forming a catastrophe risk pool along the lines of the CCRIF or PCRIP. The Philippines is already on the record in favor of such an initiative.14 Furthermore, the concept has had success in other markets: The CCRIF has provided more than a half-dozen timely payments to policyholder nations since its inception in 2007. Further, it has expanded its claims-paying capacity significantly by purchasing coverage from the international reinsurance market at highly competitive prices.

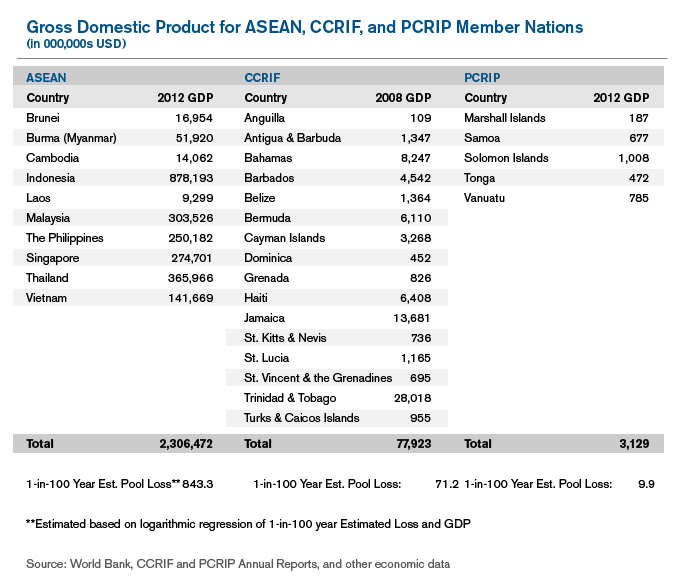

However, it would be considerably more difficult to establish a catastrophe risk pool among sizable Asian emerging markets. A potential pool, for instance, might be comprised of each of the 10 countries in the Association of Southeast Asian Nations (ASEAN). These countries and their 2012 national GDPs (in US$) are listed in the table in Figure 1, as are similar statistics for the policyholders of the CCRIF and PCRIP. With few exceptions, the ASEAN economies are significantly larger than those of their CCRIF and PCRIP counterparts—in fact, over half of the ASEAN countries have higher GDPs than the CCRIF and PCRIP taken as a whole.

As a result, the modeling and funding requirements for the pool would be of an order of magnitude higher than those for the CCRIF or PCRIP. As an example, if our hypothetical ASEAN pool was designed along similar lines to existing regional risk pools, estimated pool losses at the 1-in-100 year level might be estimated to be approximately US$850 million, using a logarithmic regression based on the loss distributions of the CCRIF/PCRIP and the GDPs of the member countries.

Figure 1: Gross Domestic Product for ASEAN, CCRIF, and PCRIP Member Nations (in $US millions)

The CCRIF was capitalized with approximately US$20 million from members and approximately US$50 million from the international donor community. This US$70 million of capital roughly equaled the 1-in-100 year loss estimate for the pool at inception. As a rough estimate, this would imply a minimum initial capitalization for an ASEAN risk pool in the range of US$700 million to US$1 billion. At this size, it would be unlikely for the international donor community to fund the majority of the initial pool surplus (as they did for the CCRIF).

An ASEAN catastrophe risk pool is also dependent upon buy-in from at least several countries in the region. For countries such as Laos and Thailand, cyclone and earthquake risks are lesser perils compared to flooding events, which historically have been far more difficult to model and insure. In addition, it would take a sizable, coordinated effort to improve the region’s catastrophe loss data—which in its current state would make it difficult to model a single peril on a region-wide basis, much less multiple threats.

As a result, though an ASEAN risk pool would likely be a significant positive force in the region, its formation may be confined to theory until solutions are found to a number of significant barriers.

A cat bond could be issued by the Philippines alone, but only provides temporary protection.

Another option for the Philippines would be to pursue catastrophe risk coverage through an ILS transaction. In this case, the model could be the cat bonds sponsored by FONDEN, the natural disaster fund of Mexico. Using the World Bank’s MultiCat platform, FONDEN issued three-year cat bonds in both 2009 and 2012, each time with a principal of approximately US$300 million.

A cat bond holds several advantages for the Philippines over a regional risk pool. The country can act without having to coordinate with its neighbors. A cat bond could also be easier for the Philippines to afford over the next several years, particularly if it could negotiate the use of aid and expertise from the donor community as part of the Haiyan relief effort. The up-front costs of structuring a cat bond tend to range from 1% to 3% of the bond face value, which would almost certainly be significantly less than the required capital contribution to forming an ASEAN catastrophe risk pool.

On the other hand, a cat bond has a defined, finite maturity. At the time it expires, should government officials choose not to renew, coverage would lapse—and there would be no pressure from the peer countries to continue the arrangement, as would exist in a pool. Cat bond sponsors also do not benefit from the ancillary benefits and services provided by a pool.

However, at this point, market conditions several years down the road may be a secondary concern. On the heels of Haiyan, the Philippines’ economy likely faces a temporary reduction in its ability to recover from severe catastrophes. Purchasing a cat bond with a typical coverage period of three-to-five years would provide a bulwark against the destabilizing effects of further catastrophe events during a time of increased need.

Conclusion: The way forward

Despite having a variety of techniques at their disposal to finance disaster recovery efforts, developing Asian states still have an unmet need for protection from particularly severe catastrophes such as Super Typhoon Haiyan. Sovereign catastrophe insurance offers a mechanism for countries to safeguard against these rare tail events. International development organizations can provide essential expertise and startup funds to emerging economies seeking to offload catastrophe risk.

The Philippines’ government has frequently expressed interest in sovereign catastrophe risk transfer. In the past, it has identified region-wide catastrophe risk pools and stand-alone cat bonds as potential sources of coverage. The ideal long-term scenario likely includes the use of both arrangements, but cat bonds may be the most feasible current option given the country’s current situation.

1. By comparison, economic losses from Hurricane Katrina amounted to approximately1.2% percent of U.S. GDP in 2005.

2. Budget ng Bayan (2012). Summary of Allocations, Budget by Department and Special Purpose Fund. Retrieved December 17, 2013, from http://budgetngbayan.com/summary-of-allocations/#dept.

3. Based on estimates from AIR Worldwide (as of November 15, 2013) and Willis Re (November 20, 2013).

4. The PNG has a 2014 budget of approximately US$53 billion. See also Dacanay, B.M. (July 12, 2013). Philippines President Benigno Aquino approves P2.3 trillion budget for 2014. Gulf News. Retrieved December 17, 2013, from http://gulfnews.com/business/economy/philippines-president-benigno-aquino-approves-p2-3-trillion-budget-for-2014-1.1208317.

5. World Bank (December 30, 2011). World Bank releases US$500 million to assist Philippine government address impacts of devastating storm. Press Release no. 2012/232/EAP. Retrieved December 17, 2013, from http://bit.ly/18RWbyY.

6. World Bank (November 18, 2013). World Bank Group supporting Philippines typhoon reconstruction with $500 million financial package. Press Release 2014/192/EAP. Retrieved December 17, 2013, from http://www.worldbank.org/en/news/press-release/2013/11/18/world-bank-group-supporting-philippines-typhoon-reconstruction-with-500-million-financial-package.

7. Cummins, J.D. & Mahul, O. (2008). Catastrophe Risk Financing in Developing Countries: Principles for Public Intervention.” World Bank.

8. PR Newswire. National Catastrophe Insurance Fund of Thailand: Companies in Thailand Take Out 3,745 Catastrophe Insurance Policies. Retrieved December 17, 2013, from

10. Asian Development Bank (2013). Investing in resilience: Ensuring a disaster-resistant future.

11. Lok-sin, L. (September 20, 2013). Interior minister in favor of buying disaster insurance. Taipei Times. Retrieved December 17, 2013, from http://www.taipeitimes.com/News/taiwan/archives/2013/09/20/2003572588.

12. Artemis.bm (April 26, 2011). Philippines still investigating the use of catastrophe bonds. Retrieved December 17, 2013, from http://www.artemis.bm/blog/2011/04/26/philippines-still-investigating-use-of-catastrophe-bonds/.

13. Ernst & Young (2013). 2013 Asia-Pacific Outlook: Where to go from here?

14. Artemis.bm (September 4, 2012). Philippines want to emulate the Caribbean Catastrophe Risk Facility in Asia. Retrieved December 17, 2013, from http://www.artemis.bm/blog/2012/09/04/philippines-want-to-emulate-the-caribbean-catastrophe-risk-insurance-facility-in-asia/.